Life insurance is a crucial financial tool, but understanding the associated costs over time can be complex. Three primary factors influence the cost of life insurance: the sum insured, the type of premium and how these change over time.

While it may make sense to review sums insured and revise covered amounts as your position changes over time, it is beneficial in seeking advice as to whether this is your best option, as ultimately this will be different for everyone.

In this article we explore the remaining two factors; the key differences between premium types, and how these change over time. This article then addresses the way insurer’s will label premiums from moving forward.

Stepped vs. Level Premiums (Pre December 2024)

Stepped Premiums

- Based on your age each year: as you get older premiums reflect the higher risk associated with making a claim.

- Annual Increases: The cost of your policy increases in steps, usually at the time of your policy anniversary.

- Lower Initial Cost: The starting premium is typically lower than level premiums. This can be an attractive entry point. It is also beneficial to consider premiums changes as you get older.

Tip: Check your Insurance quote for a projection of premiums over time.

Level Premiums

- Spreading the cost increases: Level premiums typically spread the cost increases across a number of years.

- Consistent Payments: The premium remains relatively stable over a specific period.

- Higher Initial Cost: The initial cost is generally higher than stepped premiums. Depending on how long you hold your policy, cost may be lower at a point in the future.

Tip: Check your Insurance quote for the ‘cross over’ point to compare stepped versus level.

Whether you choose stepped or level premiums, it is important to understand in either case, the cost can increase periodically.

Factors Affecting Premium Changes

Regardless of the premium type, several factors can influence changes in your insurance costs over time:

- Market Conditions: Economic fluctuations and claims rates can impact premium adjustments.

- Policy Term: The length of your policy can affect premium stability.

- Coverage Amount: Increasing your coverage will naturally lead to higher premiums.

- Policy Features: Additional riders or benefits can influence the overall cost.

- Health and Lifestyle: Changes in your health or lifestyle habits may trigger premium adjustments.

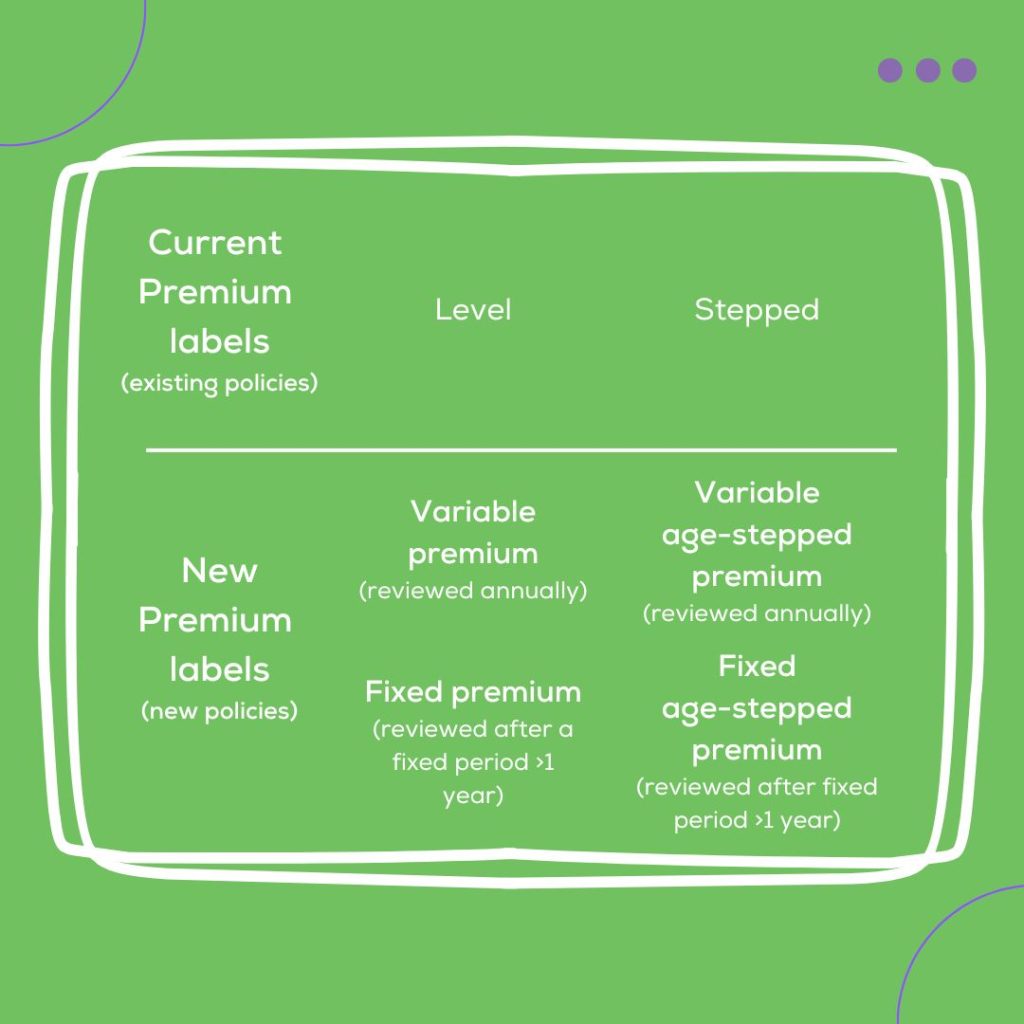

Changes to Insurance Premium Labels (Post December 2024)

To enhance consumer understanding, Life insurers in Australia will be adopting new premium labels from December 2024:

These changes are designed to make it easier to understand the type of premium applicable to you cover.

If your cover was taken out before these changes (Pre-December2024) you are unlikely to be affected. New policies from December 2024 will reflect the new premium labels.

It is important to note that each insurer may offer slightly different choices or variations to the above labels.

Making Informed Decisions

A qualified Financial Adviser can help you to determine the cover that is right for you, as well as assist in selecting a policy that takes into consideration:

- Financial Goals: Your policy should align with your long-term financial objectives.

- Risk Tolerance: Your comfort level with potential premium increases should be assessed.

- Budget Constraints: An evaluation on your ability to meet future premium payments.

- Professional Advice: Consulting with our team will help you to discuss your specific needs.

By understanding the nuances of the different premium types, as well as the upcoming changes, you can be better equipped to make informed decisions about your personal insurance coverage and protect your loved ones’ financial future.